Taxable Income, Tax-Deferred, and Tax-Advantage

Photo by The New York Public Library on Unsplash

Author: PaZoo

About 3 minutes read.

The only reason why I want to write this is to share my own experience. When I started working, I was not aware of any of these, and I basically never thought about them or reviewed them until later. I hope this could be a wake up call for those that started working, and making some earned income to think about these since tax does impact your take-home $, but do not take it negatively, they are also the vehicle for public good and pay for our infrastructure, social benefits, and society, to run our government and business, and create job opportunities, etc. It is reciprocal.

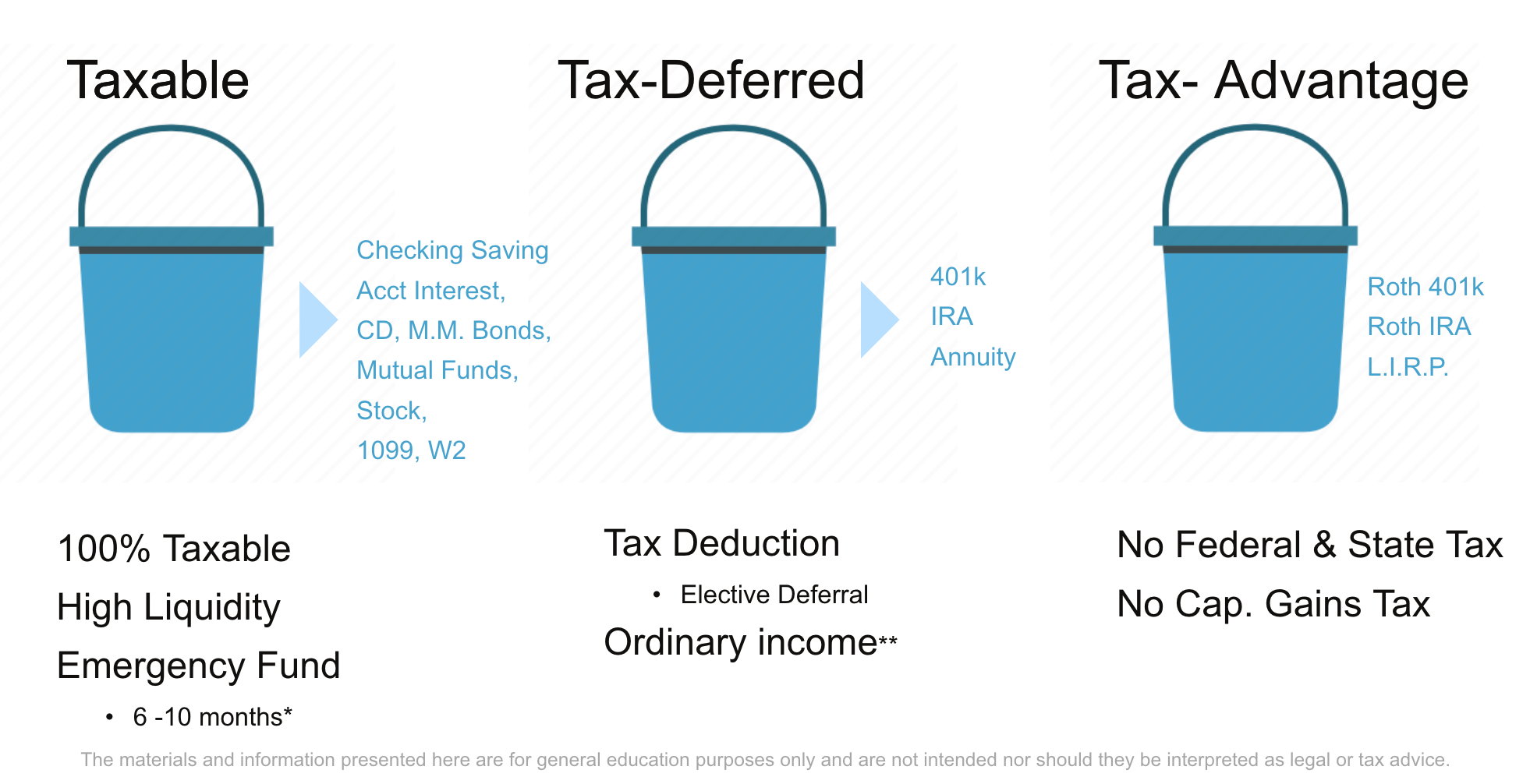

AFAIK, there are 3 tax categories today most people will encounter. They are Taxable Income, Tax-Deferred, and Tax-Advantage respectively.

What do they mean? Generally speaking, it means

Taxable Income - tax every year

Tax-Deferred - instead of tax every year, they are deferred and tax later

Tax-Advantage - tax now, and no tax later

Basically, tax needs to occur once somewhere in the live cycle when new money (earned) or assets are generated from existing money or assets (e.g. interest, capital gains on equity, property appreciation, etc.)

Here are some examples for each category for individuals (note: to simplify the examples, here, we exclude Schedule C Profit/Loss for business entities).

|

The most common ones are Taxable Income which is your salary from W-2 wages, or 1099-MISC, or 1099-DIV or 1099-INT forms. Generally speaking, your wages, interest or dividends earned on savings, CDs or stocks.

Tax-deferred usually shows up when you contribute to a qualified retirement plan such as a Traditional IRA, 401(k)/403(b) plan, or Annuity.

The 3rd one, Tax-Advantage (aka Tax-Free) usually shows up on Roth IRA, Roth 401(k), or L.I.R.P (Life Insurance Retirement Plan). (Note: I only list the most common assets/securities/plans that I am aware of here for each tax category for educational purpose only)

Different tax categories mean different tax planning and financial goals for individuals. Based on your taxable income, you may want to contribute a portion from your earned income for your retirement plan such as 401(k)/403(b) or Traditional IRA via elective deferral. Others may rollover from an existing qualified plan to another one without materializing their gain/loss. The advantage for tax-deferred allows you to contribute pre-tax dollars in a qualified retirement plan (investment), and because they are pre-tax $, it is not taxed now but in the future, so the initial investment is higher as opposed to after-tax $, and it also lowers your gross income for that year. However, the contribution is still subject to FICA (social security and Medicare taxes). Here is an example of pre-tax dollar versus after-tax dollar and their potential impact on earnings.

and when they are withdrawn after age 59 ½ for example,

This does NOT mean pre-tax or after-tax is better. My point here is tax planning. While you are working smart and hard, don’t forget to do a financial health checkup from time to time, and spend time to understand your own situation and financial goal for the long run (at different ages and milestones). For example, will your income decrease or increase after age 50? Will you still have income between age 59 ½ and 65? What could that be such as wages, rental income, business income, investment income, etc.? and don’t forget to include Social Security retirement benefit (which is taxable depending on your income) when you reach 65 and Required Minimum Distribution (RMD) after age 70 ½ or 72. Every individual situation varies and yourself knows the best of your own goals and plans. Now, you are aware of these, it is time to do your homework and due-diligence. You could always consult with a qualified tax professional and financial planner to review your financial goal, or obtain some advice as you see fit.

Reference

IRS Publication 525 - https://www.irs.gov/pub/irs-pdf/p525.pdf

IRS Retirement Plans Definitions - https://www.irs.gov/retirement-plans/plan-participant-employee/definitions

FICA - https://www.ssa.gov/thirdparty/materials/pdfs/educators/What-is-FICA-Infographic-EN-05-10297.pdf

Required Minimum Distribution - https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

%20featuring%20a%20symbolic%20scene%20with%20a%20group%20of%20diverse%20individuals%20and%20families%20interacting.webp)

Comments

Post a Comment